On March 28, 2024, the Department of Health and Human Services (HHS), together with the Department of Labor (DOL) and the Department of the Treasury (collectively, the “federal agencies”), released the Short-Term, Limited-Duration Insurance and Independent, Noncoordinated Excepted Benefits Coverage Final Rules (“final rules”).

The federal agencies released these final rules to increase consumer awareness by helping consumers easily differentiate coverage under fixed indemnity excepted benefit policies and Short-Term, Limited-Duration Insurance (STLDI) from comprehensive health coverage in compliance with the Affordable Care Act (ACA). The final rules revise the definition of STLDI and limit the length of STLDI policy contracts and renewals to a maximum of 4 months. Additionally, these final rules require an expanded consumer notice for both STLDI and fixed indemnity insurance plans.

Read on for more information detailing how the final rules impact employer-sponsored benefits.

Fixed Indemnity Excepted Benefits

Excepted benefits are exempt from certain federal consumer protections, including certain ACA mandates, such as required coverage for preventive care, prohibition of lifetime and annual dollar limits on essential health benefits, prohibition of preexisting condition exclusions, and waiting period limits.

Hospital indemnity or other fixed indemnity insurance are “excepted” under federal regulations if all of the following conditions are met:

- The benefits are provided under a separate policy, certificate, or contract of insurance.

- There is no coordination between the fixed indemnity benefits and any exclusion under any group health plan maintained by the same employer plan sponsor.

- The benefits are paid for an event without regard to whether benefits are provided for such event under any group health plan maintained by the same employer plan sponsor.

Specified Disease Coverage: For clarity, coverage for a specified disease or illness only (such as cancer-only and critical illness policies) are “excepted” benefits when they satisfy the conditions outlined above. However, specified disease coverage policies are not considered fixed indemnity coverage. As such, specified disease coverage policies are not affected by these final rules.

Additionally, under existing regulations, hospital indemnity and other fixed indemnity insurance in the group market must pay a fixed dollar amount per day (or other period) of hospitalization or illness, regardless of the amount of expenses incurred, to be considered an excepted benefit.

As with other forms of excepted benefits, fixed indemnity excepted benefits coverage does not provide comprehensive health coverage. Rather, its primary purpose is to provide income or wage replacement benefits that can be used to cover out-of-pocket expenses not covered by ACA-compliant comprehensive health coverage or to offset non-medical expenses (e.g., mortgage or rent) following a health-related event, such as a period of hospitalization or illness. Benefits under this type of coverage are paid in a flat or “fixed” cash amount. Moreover, benefits are provided at a pre-determined level regardless of the actual amount of health care costs incurred by the individual.

Although not addressed in these final rules, the federal agencies emphasized in the preamble to the final rules they remain concerned when employers choose to offer a “package” of coverage options that includes a non-excepted benefit plan that provides minimal coverage (such as coverage only for preventive services) plus fixed indemnity benefits coverage that provides benefits associated with a broad range of items and services for which the other coverage maintained by the employer excludes benefits.[1] The federal agencies intend to address these issues in future rulemaking. The federal agencies emphasized in the preamble to the final rules that employers should not make any inferences from the delay in finalizing these components of the rules. The federal agencies further reiterated that so-called fixed indemnity policies that are designed with a fee schedule that varies based on the nature of the item or service received likely do not qualify as an excepted benefit. As such, these plans are subject to the various ACA requirements, including, but not limited to, the prohibition on lifetime or annual dollar limits.

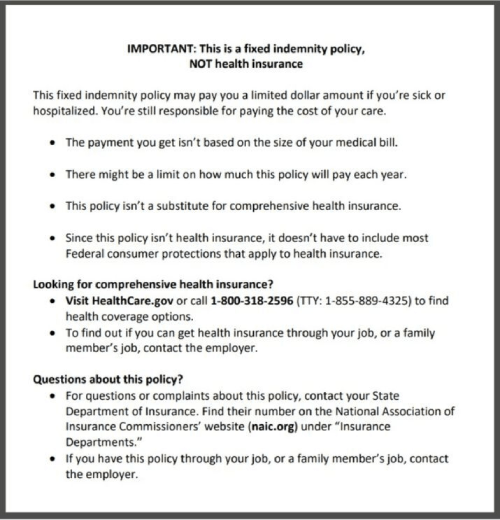

Fixed Indemnity Excepted Benefits Consumer Notice

These final rules require a consumer notice to be provided to employees when offering fixed indemnity excepted benefits coverage in the employer-sponsored group market.

The rules underscore the view of the federal agencies that these notices “will help ensure that all consumers, including those in underserved communities, have the necessary information to make an informed choice after considering and comparing the full range of health coverage options available to them.”

Fixed indemnity excepted benefit insurers are required to prominently display a notice in at least 14-point font on the first page of any applicable marketing, application, or enrollment materials (or re-enrollment materials) that are provided to participants at or before the time participants are given the opportunity to enroll (or re-enroll) in the coverage.

This consumer notice requirement for fixed indemnity excepted benefits coverage in the group market is applicable to plan years beginning on or after Jan. 1, 2025.

Model Language for Fixed Indemnity Excepted Benefits Consumer Notice

See below for the model notice language for group fixed indemnity excepted benefit coverage:

Reminder: This group fixed indemnity coverage model notice language must be prominently displayed by the plan insurer in at least 14-point font on the first page of any applicable marketing, application, or enrollment materials (or re-enrollment) materials that are provided to participants at or before the time participants are given the opportunity to enroll (or reenroll) in the coverage.

Short-Term, Limited-Duration Insurance (STLDI)

Short-Term, Limited-Duration Insurance (STLDI) is a type of health insurance coverage sold by health insurers that typically fills temporary gaps in coverage that may occur when an individual is transitioning from one plan or coverage to another, such as when an individual changes jobs.

STLDI is exempt from the consumer protections and requirements for comprehensive medical coverage under the Affordable Care Act (ACA), including the prohibition on discrimination based on health status, prohibition of preexisting condition exclusions, and the prohibition on lifetime and annual dollar limits on essential health benefits.

Individuals who enroll in STLDI are not guaranteed these consumer protections under federal law, which can be particularly problematic when the differences between STLDI and ACA-compliant comprehensive coverage are not readily apparent to consumers. As a result, consumers might be underinsured when they enroll in STLDI and may end up forgoing needed, routine medical treatment, and exacerbating chronic medical conditions because of limited benefits or high cost-sharing responsibilities, according to the final rules.

These final rules amend the federal definition of STLDI to limit the length of the initial contract term to no more than three months and the maximum coverage period to no more than four months, including any renewals or extensions.

Currently, the rules permit an initial STLDI contract term of fewer than 12 months and a maximum total coverage period of up to 36 months, including renewals and extensions.

The new definition for STLDI is consistent with the group market rules regarding the 90-day waiting period provision under the ACA and with STLDI’s traditional role of serving as a temporary coverage for individuals changing jobs, and transitioning from one employer-sponsored ACA-compliant group health plan to another. Aligning the maximum duration of an STLDI policy to no more than 4 months with the period federal law expressly permits as a bona fide employment-based orientation period most appropriately reflects STLDI’s traditional role to fill temporary gaps in comprehensive coverage, according to the federal agencies in the preamble to the final rules.

These final rules apply to new STLDI policies sold or issued on or after September 1, 2024. Any STLDI policies sold or issued before September 1, 2024 will not be subject to these changes in the final rules.

Finally, the final rules ban a practice referred to as “stacking,” where the same insurer issues multiple STLDI policies to the same policyholder within a 12-month period.

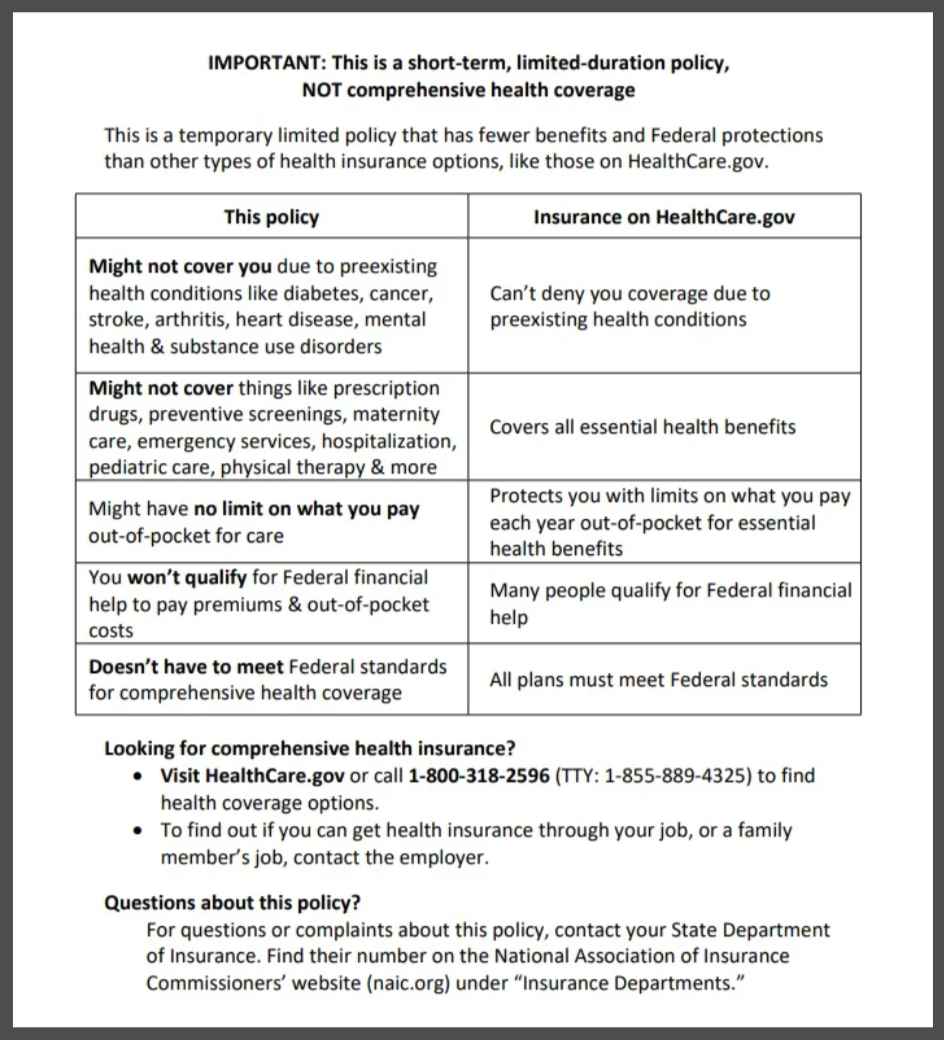

STLDI Consumer Notice

These final rules amend the federal notice standard to assist consumers in differentiating between ACA-compliant comprehensive coverage and STLDI and get information on their health coverage options.

STLDI insurers will be required to display a notice on the first page (in either paper or electronic form, including on a website) of the policy, certificate, or contract of insurance, and in any marketing, application, and enrollment materials (including re-enrollment materials) provided to individuals at or before the time an individual has the opportunity to enroll (or re-enroll) in the coverage, in at least 14-point font.

This consumer notice requirement for STLDI will apply to coverage periods (including renewals and extensions) beginning on or after September 1, 2024.

Model Language for STLDI Consumer Notice

See the language below for the updated model notice language for STLDI insurers:

Reminder: This STDI model notice language must be prominently displayed in at least 14-point font on the first page of the policy, certificate, or contract of insurance—including for renewals and extensions—and included in any marketing, application, and enrollment (or re-enrollment) materials.

Tax Treatment for Amounts Received from Fixed Indemnity Insurance & Certain Other Arrangements

The proposed rules, released on July 7, 2023, included proposed amendments addressing the taxation of fixed indemnity (and other similar wellness indemnity plans) arrangements. Specifically, the proposed rules clarified that payments from employer-provided fixed indemnity plans (and other similar plans) are not excluded from a taxpayer’s gross income if the amounts are paid without regard to the actual amount of any incurred medical expenses.

However, the final rules confirmed that the federal agencies are not finalizing these proposed amendments at this time to allow them additional time to study and address the comments received and release rules in the future. Specifically, commenting stakeholders raised the concern that these amendments, if finalized, would require additional guidance from the federal agencies regarding collecting and paying employment taxes on some or all of the amounts paid through accident or health insurance that are not excluded from gross income, and proper reporting of such amounts on an employee’s Form W-2. Commenters also requested further clarification on how incurred medical expenses must be substantiated.

Notwithstanding the delay in finalizing these rules, the IRS reiterated that employers should not draw any inference regarding whether the IRS agrees with the comments. As noted in our prior article accessed here, the IRS has issued a series of memoranda over the last several years expressing the agency’s stance on the taxation of payments from fixed indemnity plans.

Finally, the final rules remind employers that benefit amounts received through fixed indemnity plans are not taxable if premiums for the coverage are paid on an after-tax basis. Employers may be able to avoid many of the practical concerns relating to benefits that do not meet the criteria to be excluded from gross income by ensuring that employees pay premiums for fixed indemnity plans (and other similar plans) on an after-tax basis.

Employer Impact

Employers that offer fixed indemnity plan benefits on a group basis to their employees should be aware of the expanded consumer notice requirement, which their plan insurers are generally responsible to comply with for plan years beginning on or after Jan. 1, 2025. Employers might also consider a concerted communication effort to include the model notice language in their own enrollment guides to ensure employees clearly understand the difference between fixed indemnity plans and ACA-compliant group health plan coverage.

Furthermore, for those employers currently offering STLDI coverage to employees (generally employers in service industries, such as hospitality or food service, with minimum-wage workers), they should be aware of the revised time limits for these policy contracts and renewals, set to change on September 1, 2024. These employers should also be aware of the expanded consumer notice requirement for STDLI for coverage periods (including renewals and extensions) beginning on or after September 1, 2024.

eBen and Risk Strategies are closely tracking developments in this space and will provide updates when available. Contact us directly here.

[1]The federal agencies “explained they are concerned that some employers are attempting to circumvent the Federal consumer protections and requirements for comprehensive coverage that otherwise apply to group health plans” with this approach.

The contents of this article are for general informational purposes only and eBen|Risk Strategies Company makes no representation or warranty of any kind, express or implied, regarding the accuracy or completeness of any information contained herein. Any recommendations contained herein are intended to provide insight based on currently available information for consideration and should be vetted against applicable legal and business needs before application to a specific client.